.png)

Introduction

Over the past half century, medical devices have transformed the practice of medicine through a series of fundamentally physical breakthroughs. Advances in materials, miniaturized electronics, and battery technology made it possible to build implantable pacemakers that could regulate cardiac rhythm continuously inside the body. Improvements in membrane science and fluid dynamics enabled dialysis machines to replicate the filtration function of the kidney. Ventilators combined advances in mechanics, control systems, and oxygen delivery to sustain patients through respiratory failure.

In each case, the value was rooted in engineering, materials, and form factor, in what the hardware could physically do that nothing else could. Software played an important role, but it operated primarily as a layer of control, optimization, and safety on top of a fundamentally hardware-driven system.

That relationship is now beginning to shift. Across parts of the industry, the axis of competition is shifting from hardware to software. This is already visible in areas such as retinal imaging, where two cameras may capture comparable images, but the systems built on top of those images are increasingly where value is created. AI can enable screening for conditions such as diabetic retinopathy, and emerging work suggests the same data may support broader insights into cardiovascular and neurological health. The hardware remains essential, but the differentiation increasingly lives in software.

This has profound implications for how medical device companies are built and how they create venture-scale outcomes. This paper examines those implications. We begin with the historical return profile of medical device venture capital — a category that has produced clinically important companies but relatively few billion-dollar exits. We then examine why, and argue that as the axis of competition shifts from atoms to algorithms, the companies that clear the same regulatory and commercial hurdles as their predecessors can access far larger outcomes on the other side.

The State of the Medical Device VC Markets

Today, the U.S. medical device market is an estimated roughly $200 billion annually. Against total U.S. healthcare spending of approximately $5.3 trillion, devices represent nearly 4% of the healthcare economy. Despite this scale and clinical importance, venture investment in the category has historically been modest.

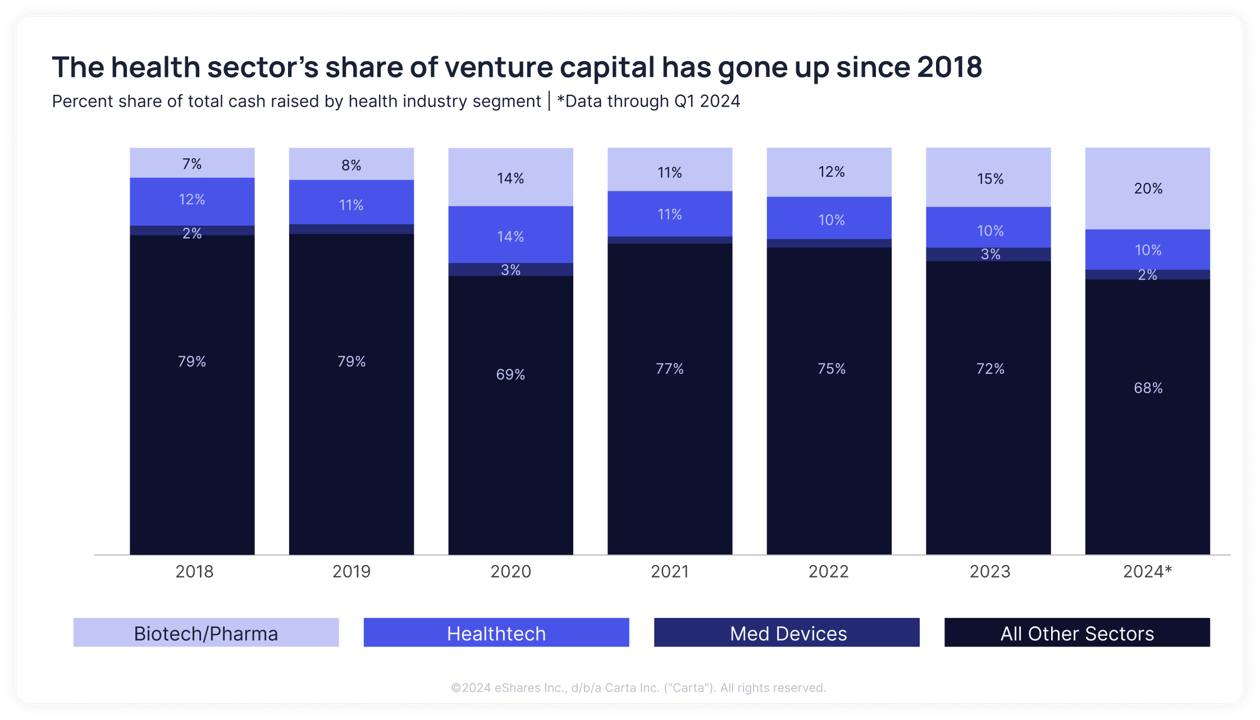

Data from Carta shows that while the health sector's overall share of venture capital has grown meaningfully since 2018 — rising from roughly 21% to over 32% of total cash raised — medical device startups have captured only a narrow slice of that growth. Biotech and pharma account for the majority of healthcare venture dollars and have seen their share nearly triple over the same period, while medical devices have remained largely flat at roughly 2–3% of health sector investment.

The concentration of healthcare venture capital in biotech and pharma reflects the category's historical return profile as much as its clinical importance. The U.S. medical device market overall is highly concentrated, with a small group of large incumbents accounting for the majority of revenue, while startups comprise a relatively limited market share.

Yet despite this concentration, innovation is largely driven by a broad ecosystem of startups. Incumbents continue to invest in new technologies, but they often prioritize lower-risk opportunities, which leaves gaps in the market that startups focus on, competing to develop differentiated products that are both clinically effective and commercially viable.

The category’s limited venture share is not because device companies are less important. It is because the path to venture-scale outcomes in medical devices is shaped by structural constraints: bounded markets, early manufacturing complexity, expensive evidence generation, and adoption cycles that move at the speed of clinical workflow rather than product launches.

The result is a category that produces many strong, clinically meaningful companies — but relatively few that reach billion-dollar venture-backed valuations.

The central question for investors is therefore not whether the distribution follows a power law, but whether the right tail is large enough. In other words, does the category reliably produce enough billion-dollar outcomes to justify significant capital allocation relative to other venture sectors?

Looking at venture-backed medical device companies founded and exited since 2000 provides a clearer picture of how venture outcomes in the category actually materialize.

Historically, venture-backed medical device exits have followed a recognizable pattern. The five themes below characterize what that track record has looked like and set the stage for what may be shifting.

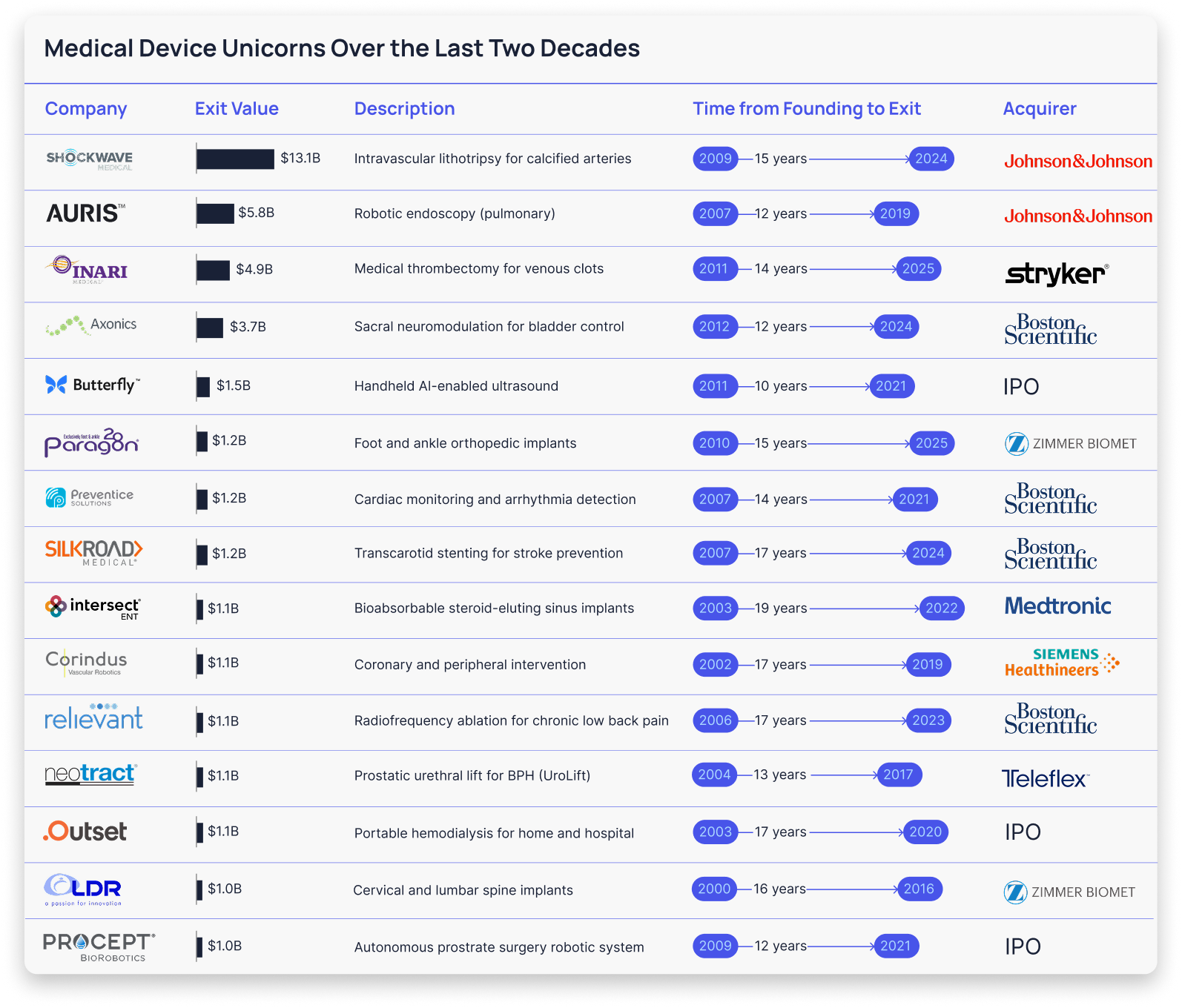

01. Venture-backed medical device unicorns are historically rare.

Fewer than twenty venture-backed medical device companies have achieved exit valuations above $1 billion over the past two decades, compared to hundreds of unicorns across all sectors.

02. Most exits have clustered around the low end of the billion-dollar range.

The majority of outcomes fall in the $1.0–$1.5 billion range, with only a handful of exits exceeding $3 billion. Even these headline values frequently include earnout components tied to.

03. Strategic acquisition has dominated exit pathways.

The vast majority of companies exit through M&A rather than public markets. This reflects a structural feature of the industry: once technical and clinical risk has been reduced, incumbent device companies are often better positioned to scale a product globally through established sales channels, clinical education programs, and manufacturing infrastructure.

04. Time horizons are long.

Most successful device companies take more than a decade to reach exit, with many requiring 12–17 years from founding to acquisition or IPO. These timelines can be challenging for early-stage venture investors, whose fund cycles often assume faster capital recycling.

05. Most unicorn exits have come from interventional devices.

The majority of billion-dollar exits involve interventional technologies rather than diagnostics, often in high-margin therapeutic specialties. Many of these companies introduced entirely new treatment approaches. These companies succeeded by introducing technologies that reshaped clinical workflows and expanded interventional categories.

Taken together, these patterns help explain the venture capital allocation gap. Medical devices clearly create enormous clinical value and durable businesses, but historically the category has produced relatively few venture-scale outcomes compared with other sectors of venture capital.

While traditional hardware-based medical device unicorn outcomes were relatively rare, there have been emerging examples of venture-scale outcomes in adjacent models. One is software as a medical device (SaMD), where companies generate clinical insight from existing data streams without introducing new hardware. HeartFlow provides a clear example. Founded in 2007, the company developed software that uses AI and computational modeling to analyze coronary CT scans and non-invasively assess blood flow in the heart. In August 2025, HeartFlow went public at an approximate $2.3 billion valuation, demonstrating that software-driven approaches can achieve scale within regulated medical technology.

A second model has combined devices with broader technology-enabled services. Livongo built its diabetes platform around a connected glucometer, using the device to anchor a chronic disease management offering. More recently, Hinge Health followed a similar approach in musculoskeletal care, combining an FDA-cleared device with coaching, therapy, and digital care pathways. Both companies reached multi-billion-dollar outcomes by expanding beyond the device itself into a broader portion of the care journey.

These examples represent emerging medical device sub-categories that highlight an important idea: the largest outcomes in medical devices often come when companies extend beyond a single product and access broader sources of value. Companies like Aidoc ($370M+ raised) and Iterative Health ($190M+ raised) have matured from AI-enabled tools into infrastructure platforms, positioning themselves for venture-scale returns by owning entire segments of the clinical workflow.

Yet these cases remain exceptions to a broader pattern. To understand the medical device market’s trajectory, it helps to examine the structural factors that have historically constrained it:

- Market sizes are often narrower, with products tied to specific procedures or clinical specialties.

- Regulatory timelines are long, with many years required to generate evidence and reach commercialization.

- Regulatory risk can be binary, concentrating large amounts of capital behind pivotal approvals.

- Reimbursement pathways are complex, and companies with strong clinical value may still struggle to secure consistent payment without establishing new billing codes or coverage policies.

- Workflow adoption requires education and behavior change, often more so than pharmaceuticals, as clinicians must integrate new devices directly into procedures and care pathways.

These constraints have historically limited the number of venture-scale outcomes in the category. Understanding how they shape company trajectories is essential to understanding why medical devices have evolved the way they have — and what may be changing in the AI era.

How AI Reshapes the Path to Scale

The historical dynamics of medical device venture outcomes are shaped by real structural constraints. Regulatory pathways are long and capital-intensive. Clinical evidence must be generated over multiple years. Reimbursement remains complex and often uncertain. Adoption depends on integration into clinical workflows that change slowly. None of these constraints are disappearing.

At the same time, a broader shift is occurring across technology markets. As artificial intelligence reduces the cost of building software and delivering many services, value is increasingly accruing to what remains scarce. In healthcare, that scarcity often sits at the intersection of regulated products, proprietary data, and real-world deployment. In that context, the characteristics that have historically made medical device companies difficult to build may increasingly become sources of advantage. There is a growing premium on doing hard things.

The implication is not that medical devices suddenly become simple to build. The process remains multi-year and capital intensive, but with AI it is becoming faster and more efficient at key points along the way. More importantly, the payoff from building a successful device company is increasing. The same path through regulatory approval and commercialization can now lead to outcomes that are materially larger than in prior generations of device companies.

Medical devices encompass a wide range of subcategories — from diagnostics and screening to interventional tools, monitoring systems, and implantables. We believe artificial intelligence will reshape each, but these shifts will not affect all subcategories equally or on the same timeline. We expect the most significant near-term impact to concentrate in diagnostics, where the ability to extract and interpret richer clinical insight from existing data streams aligns most naturally with AI’s core strengths. While our analysis is most grounded in diagnostics, the following shifts reflect dynamics that are beginning to reshape the broader category and extend to the full range of medical device innovation.

1. Expanding total addressable markets

Historically, most medical devices were tightly coupled to a single procedure or diagnostic use case. A device was built to solve a specific clinical problem, and its market was bounded accordingly. This constraint has been one of the primary reasons why many successful device companies have reached a natural ceiling in scale.

AI begins to change this by allowing multiple clinical insights to be extracted from the same underlying data stream, and in some cases by enabling entirely new biological signals to be measured that were previously inaccessible. A single sensing platform can support a growing set of applications over time, as new models are developed and validated. Instead of building a new device for each adjacent market, companies can expand by layering additional capabilities onto an existing system.

Retinal imaging provides a clear example. A system initially deployed for diabetic retinopathy screening can, with additional algorithms, be extended to assess cardiovascular risk or detect early signs of neurological disease. The underlying hardware and data acquisition remain the same, but the set of clinical questions the system can answer expands. Optain, an Aegis co-founded company, reflects this approach, where a single platform can evolve from a point solution into a multi-indication diagnostic system. Each additional indication builds on the same infrastructure, allowing the company to expand its addressable market without rebuilding the core system.

2. Tapping into higher-value clinical workflows

AI also changes who can use a device and how it is used within care delivery. Many diagnostic technologies have historically required trained specialists to operate and interpret. As a result, their use has been constrained to specific settings and workflows.

By embedding guidance and interpretation into the system, AI allows less specialized users to perform tasks that previously required significant expertise. This expands the range of clinical settings in which a device can be deployed and increases its role within the care pathway.

A useful analogy is the evolution of smartphone cameras. Hardware improvements have been important, but much of the value comes from software that automatically adjusts for lighting, focus, and composition, allowing an amateur user to produce a high-quality image. A similar dynamic is beginning to emerge in medical devices. Systems can guide acquisition, standardize output, and provide interpretation, allowing generalists to perform tasks that previously required specialists.

In the case of retinal imaging, this means that screening and risk assessment can move beyond specialist settings and into primary care or even consumer environments. The device is no longer limited to a narrow diagnostic workflow. It becomes a broader entry point into care, participating in earlier stages of detection and expanding its relevance within the system.

This same dynamic is extending with advancements in digital medical devices. Care is moving into the home and other lower-cost settings through connected monitoring and remote diagnostics, while devices are increasingly used to manage conditions over time rather than at a single point of diagnosis. Continuous data collection and earlier intervention can reduce complications, avoid hospitalizations, and lower the total cost of care, while improving patient outcomes.

This shift allows devices to access higher-value clinical workflows. Rather than simply generating data, they contribute to decision-making and intervention. The result is deeper integration into care delivery, greater economic value within the healthcare system, and a dynamic that is not limited to any single subcategory. From monitoring systems tracking physiology remotely to interventional tools like surgical robotics that enhance procedural reach, this transformation is reshaping the entire medical device category.

3. Building compounding data advantages

A third shift emerges from the interaction between hardware, data, and AI. Devices that are deployed in real-world settings generate proprietary datasets that can be used to improve model performance and expand capabilities over time. When a company controls both the data acquisition and the intelligence layer, it can build a feedback loop between usage and improvement.

This is structurally different from many software-only approaches. Software-as-a-medical-device companies often rely on data generated by systems they do not control, such as imaging datasets collected by hospitals or third party equipment. While strong businesses can be built on this model, the path to compounding defensibility is different for companies that control their own data acquisition.

In contrast, a device that captures its own data creates the opportunity to build a proprietary dataset tied to real-world usage and outcomes. As the system is deployed, the dataset grows, models improve, and the product becomes more capable. Over time, this creates a compounding advantage. The system is not only embedded in workflow, but also continuously improving based on data that competitors may not be able to replicate.

Wavelet, another company we launched, illustrates this model. Wavelet uses AI to monitor fetal brain signals through the mother’s abdomen, replacing the often-ambiguous heart rate monitoring traditionally used to detect distress during labor.

By extracting neurophysiological signals non-invasively, the system provides real-time insight to reduce avoidable brain injuries and unnecessary C-sections. Each birth monitored by the system generates new data that improves the accuracy of the underlying models. As the dataset grows, the device evolves from a standalone product into an increasingly valuable piece of care infrastructure.

In this context, hardware becomes more than a delivery mechanism. It becomes a means of accessing and controlling the data layer that underpins long-term differentiation.

Looking Ahead

We believe the coming decade will bring a new wave of biological transformation. Advances in sensing technologies, computational biology, and artificial intelligence are expanding our ability to measure and understand human physiology. As these tools mature, they will reshape how diseases are detected, monitored, and treated — enabling earlier intervention and allowing people to live healthier, longer lives.

We are optimistic about what this means for the future of medicine. At Aegis, we look forward to partnering with the next generation of AI-native scientist-entrepreneurs building those systems.